Unlock 2024 Sales Comp Secrets: Our "Ultimate Guide to Sales Compensation" is here!Unlock 2026 Sales Comp Secrets: Our "Ultimate Guide to Sales Compensation" is here!Download Guide

Blog

Deferred Commissions: ASC 606 Impact on Sales Accounting

April 5, 2024

Key Insights

Sales commissions are a powerful tool in sales management.

However, the calculation and accounting part of sales commissions can be complicated. There are deferred commissions, accruals, ASC 606, sales commission accounting, and many more. These jargons are just the tip of the iceberg and there is more to explore.

So why is sales commission accounting so complicated? How has ASC 606 brought changes to the current accounting system? Let's find answers to all these questions and more.

In this article we will walk you through the amortization process, sales commission accounting before and after ASC 606, key changes in calculating sales commissions, how to amortize your sales commission, and some best practices for commission expense allocations.

How Amortization Works

Amortization is the process of writing down the value of an intangible asset across a period of time. It is commonly used in finance and accounting to spread out the cost of a large expense over time.

For example, a particular license costs $200 for a company with a validity period of 4 years. In traditional accounting, this ‘expense’ will be accounted for in that particular year.

But in the new accounting system this cost will be referred to as an asset and spread across these 4 years. Hence, sheets will show a $50 on the license for the next 4 years.

How ASC 606 Changed Sales Commission Accounting

Earlier there existed a lot of discrepancies in the way different companies used to handle accounting for similar transactions.

With the introduction of Accounting Standard Codification 606 (ASC606), a streamlining of accounting processes and standardization of the revenue recognition process was established.

ASC 606 is a set of accounting standards developed in collaboration between the International Accounting Standards Board (ISAB) and the Financial Accounting Standards Board (FASB).

Among its many revenue recognition policies, one significant impact was introduced on sales commission accounting.

Let us look at these changes brought about by ASC 606 in sales commission accounting:

Capitalization of Commissions

Under the new ASC 606, capitalized commissions are accounted as assets rather than a one-time expense in their balance sheet.

This is because sales commissions are tied to the contract that will bring future revenue to the company. Deferred commissions are then amortized over the expected period of the contract.

Amortization Period

Earlier sales commissions were recorded as one-time expenses in the balance sheet. Now companies spread the sales commission costs across the term of the contract.

This term can be longer or shorter depending on customer renewals, contract modification, customer satisfaction, etc.

Incremental Costs of Obtaining a Contract

Companies have additional expenses while closing a deal (obtaining a contract) from a client. This can be sales commissions, marketing expenses, legal fees, etc.

ASC 606 clearly specifies how these incremental costs must be handled in the balance sheet. Sales commission being one of these additional expenses are accounted as assets under certain conditions and amortized over the contract term.

Disclosure Requirements

ASC 606 requires the disclosure of particulars related to sales commission accounting. Companies must clarify the nature, timing, and amount of sales commissions invested, and how they were accounted for and amortized.

This clarity in sales commission accounting provides transparency in the revenue recognition process.

ASC 606 thus brought clarity on how companies accounted for their deferred commissions and transparency in how customer contracts were obtained and fulfilled.

Sales Commission Accounting Before ASC 606

ASC 606 came into effect in 2017. Until then sales commission accounting was governed by previous standards like ASC 605.

Let's look at some of the practices before ASC 606 was implemented:

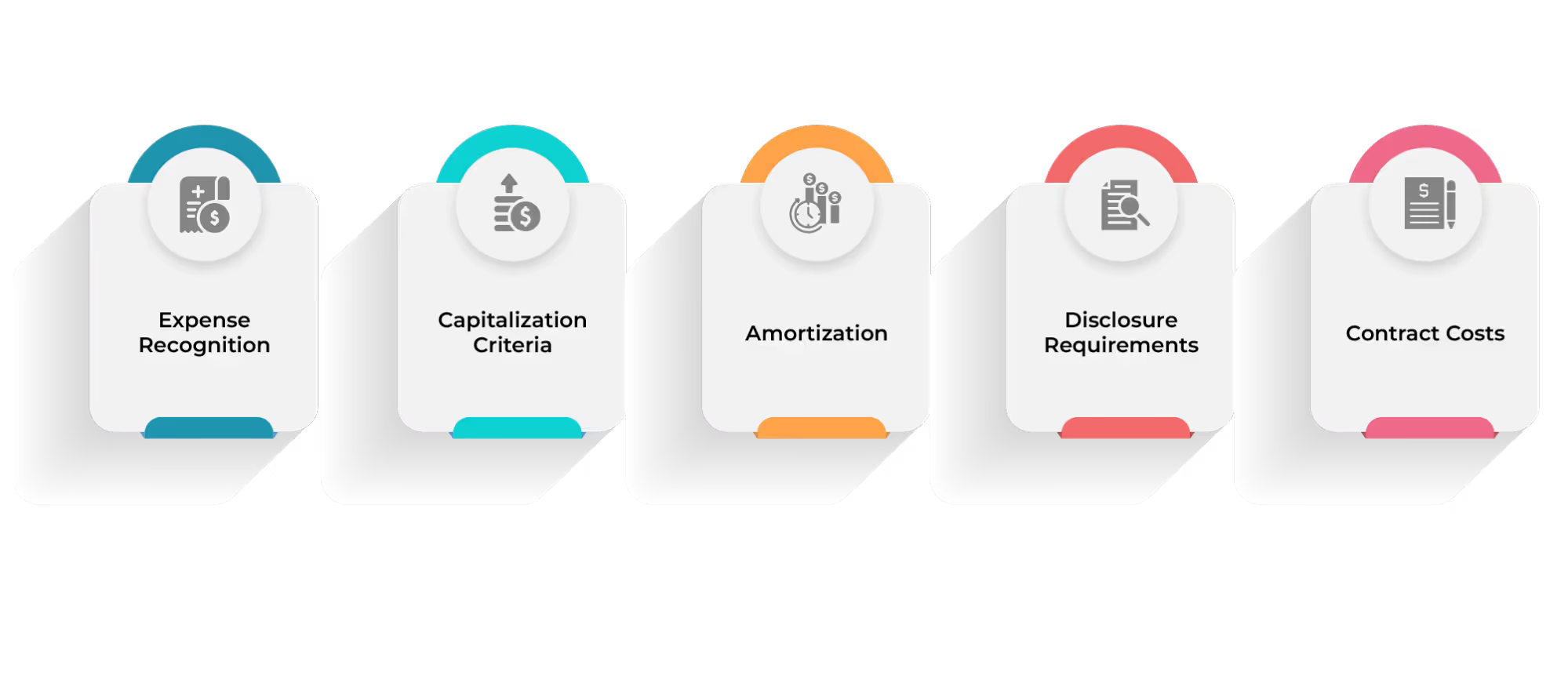

Expense Recognition

Under ASC 605, sales commissions were accounted as expenses at the same time when the revenue associated with it was recognized.

This approach is called the expense-matching principle and allows companies to match their expense with the revenue during the same period of associated revenue recognition.

Capitalization Criteria

While some companies accounted for sales commissions as expenses, others determined them as assets even before ASC 606.

However, there was less consistency in how the same sales commission was handled across different companies and industries causing varied practices and discrepancies.

Amortization

Even in situations where companies accounted their sales commissions as assets and amortized them over the contract term, there was no uniformity or standard practice.

This meant that the amortization period and method varied based on company factors and industry practices.

Disclosure Requirements

Before ASC 606 there was no standardization in the accounting disclosure requirements.

Companies disclosed particulars related to their accounting policies, revenue recognition, and expenses, and the level of detailing varied drastically.

Contract Costs

Earlier sales commissions were considered as expenses incurred in obtaining a contract. It gave less guidance on how these direct and indirect costs must be accounted for.

With ASC 606 there is more detailing, clarity, and transparency in recording and calculating sales commissions.

Before ASC 606, sales commission accounting was a haphazard process with discrepancies happening on company and industry bases. The new revenue recognition standard under ASC 606 thus has uniformity, standardization, and transparency in the accounting process.

Key Changes to Calculating Sales Commission Expenses

Businesses have taken a nuanced approach towards sales commission calculation ensuring compliance with ASC 606 while accurately reflecting the company's financial position.

From recording the cost in the balance sheet to how it is calculated, sales commission accounting has undergone a standardization that ensures uniformity in sales commission calculation in similar industries.

- To begin with, under ASC 606, sales commissions are incurred as assets rather than expenses.

- Instead of incurring the costs in the same period as the related revenue, the sales commission is spread across the contract tenure.

- The amortization of the asset has become a crucial step where companies forecast their expenses.

There are complexities added to sales commission accounting with ASC 606. Earlier sales commission accounting was a straightforward calculation that incurred it as an additional expense to the associated revenue.

Now with ASC 606, though the calculation has become complex there is more clarity and transparency in the way it is accounted for as well as uniformity across industries on its calculation.

Check out our free sales commission calculator.

How to Amortize Sales Commissions Under ASC 606

Prior to ASC 606, sales commission was accounted for as expenses in the expense matching principle.

Hence, sales commission was incurred as an expense and recorded in the same period of the related revenue.

After the implementation of the ASC 606, sales commission must be accounted as an asset and amortized across the contract term. Let us look at how the amortization process is done.

For example, a sales rep was paid a commission of $3000 for closing a deal with a contract term of 2 years (24 months). The amortization of the sales commission will account for an asset of $125 per month.

Following the new revenue recognition under ASC 606, sales commissions will be accounted:

Scheduled journal to amortize the existing book of commission paid on opportunities:

Amortizing sales commissions under ASC 606 may vary depending on the nature of the contracts, industry practices, and company-specific circumstances.

Companies should carefully consider the guidance provided in ASC 606 and consult with accounting professionals as needed to ensure compliance and accurate financial reporting.

How Long to Amortize Sales Commissions for Saas and Other Subscription Business Models

There is no universally “definite” answer as to how long to amortize sales commissions for SaaS and other subscription-based models.

Several factors come into play in determining the period. For example in a SaaS industry with subscription-based business models, the length of the contract, customer retention rate, contract renewals, expected customer relationship period, etc will define the amortization period.

In addition, businesses must also take care in ensuring compliance with the ASC 606 accounting standards to disclose their accounting policies and methods used for amortizing sales commissions in the financial statements.

Hence, the amortization period can range from several months to years.

From internal factors like business models and contracts to legal factors like accounting policies determine the appropriate amortization period for deferred commissions in SaaS and subscription-based business models.

Best Practices for Commission Expense Allocation

Businesses must incorporate some best practices to ensure accurate, transparent, and compliant commission expense allocation.

Let us look at some of these best practices in detail:

Alignment with Revenue Recognition

Ever since the ASC 606 implementation, businesses must closely adhere to the revenue recognition process and follow the standard practices associated with it to ensure clarity and transparency.

Capitalization Criteria

Businesses must determine the capitalization of commission expenses based on eligibility criteria and amortize it over the appropriate period as outlined by ASC 606.

Consistency

Similar types of contracts and transactions must be accounted for with consistent commission expense allocation methods to ensure compatibility and reliability in financial reporting.

Transparency

The financial statement must communicate and transparently disclose how commissions are allocated, capitalized, and amortized.

Regular Review

Regular review of commission expense allocation methods ensures they adhere to the revenue recognition policies and are updated with the changing business conditions.

Documentation

Maintain a clear commission expense allocation documentation that clarifies the rationale behind the chosen method, key assumptions, and other relevant calculations and analyses.

Compliance

Businesses must ensure they comply with the relevant accounting standards, regulations, and policies and stay informed about changing standards and practices on commission expense accounting.

Following these best practices will help businesses effectively allocate their commission expenses that support accurate financial reporting and comply with accounting standards.

Final Thought

With ASC 606, sales commission accounting has become a complex process that is prone to error when calculated manually.

Businesses require sales compensation automation tools that ease the tedious task of everyday accounting.

Automation tools streamline the data collection process, ensure error-free calculations, provide transparency and clarity in deferred commission accounting and ensure compliance to the changing revenue recognition regulations.

Kennect offers all these features and more with our compensation automation tool.

Our automated solution integrates across CRM, ERP, and HRIS, and provides sales leaders real time insights to make bold and quick decisions.

For more reading on sales incentives and policies, visit our blog resources.

ReKennect : Stay ahead of the curve!

Subscribe to our bi-weekly newsletter packed with latest trends and insights on incentives.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Your data is in safe hands. Check out our Privacy policy for more info

Related Articles

Address

Kennect

224 W 35th St 500 820

New York , NY 10001

(415) 799-4494

224 W 35th St 500 820

New York , NY 10001

(415) 799-4494

Contact

Phone : (415) 799-4494

Email : info@kennect.io

Social

Achivement

© 2024 Kennect - All Rights Reserved.

Privacy Policy